A full copy of this paper can be obtained from co-author, Dr. Theo Stratopoulos at the Centre of Performance Management Research and Education, University of Waterloo: tstratopoulos@uwaterloo.ca.

Introduction

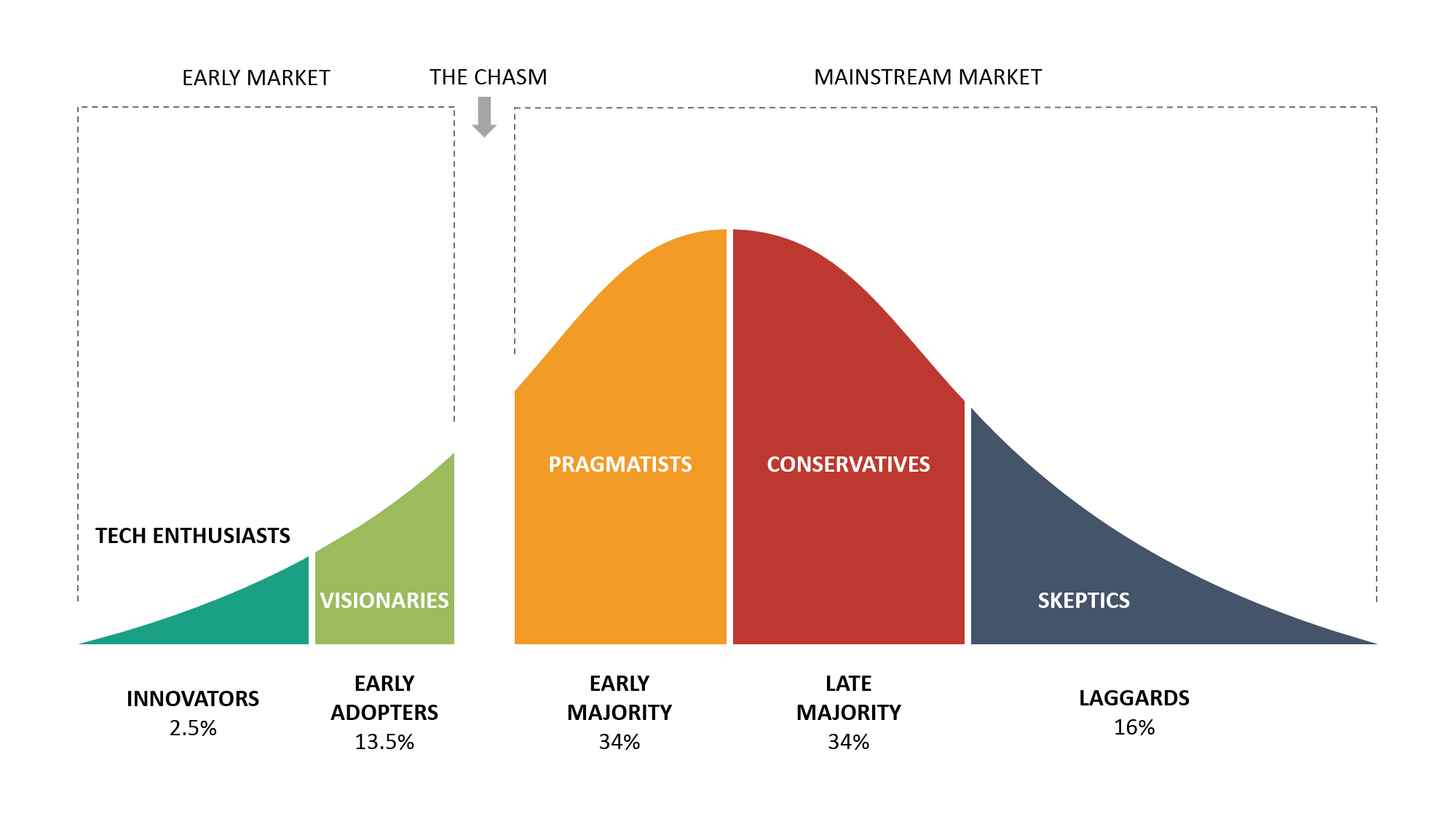

A broad consensus has arisen around the game-changing potential of Blockchain – a digital ledger technology. Nevertheless, views are mixed as to when it will reach mainstream adoption. The technology adoption cycle is well-defined. Technologies generally move through five stages: innovators, early adopters, early majority, late majority, and laggards. Of course, many fail to cross the chasm between early adoption and early majority (Figure 1).

Figure 1: The Technology Adoption Life Cycle

Despite the considerable press and industry attention surrounding Blockchain, some experts believe it could be several decades before the majority of organizations use it. Others contend that the technology is no more than five years away from majority adoption.

For investors deciding where to place their bets, a reliable determination of where Blockchain currently resides in the adoption cycle, and when it is likely to cross the chasm to majority adoption, would prove invaluable. Such estimates would also benefit firms evaluating Blockchain adoption, those interested in integrating it within the platforms they sell, governments hoping to keep pace, and researchers.

“[Adopting] firms differ only in their original beliefs that the innovation is profitable ... differences among firms in their subjective beliefs that the innovation will be profitable may be sufficient to explain the commonly observed pattern of diffusion.”

The authors’ methodology has application well beyond Blockchain. Indeed, it could be applied to any emerging technology, including, for example, the Internet of Things (IoT), Fintech or quantum computing. It might even work as a real-time predictive tool in assessing emerging technology adoption.

In this paper, the authors argue that they obtain a better estimate of emerging technology adoption (in this case Blockchain) by examining trends in web site, book title and article mentions (the traditional approach), and by analyzing voluntary and mandatory corporate disclosures and transcripts from shareholder conference calls (the novel approach). Doing so, they find that Blockchain is transitioning from the innovator to early adopter stage. This finding is further validated from the results of a Latent Dirichlet Allocation (LDA) machine learning algorithm applied by the researchers to their findings.

Assumptions/Hypotheses

The authors propose that potential technology adopters (buyers, sellers, investors, etc.) gather information before making their decision. With this information, they gauge the potential risks and advantages of moving forward and signal their intent to adopt emerging technologies. Other researchers have proposed that by examining trends in web searches and book titles, for example, it might be possible to predict when a technology is moving from the innovator and early adopter stages to majority adoption.

Web searches, articles and book titles, however, tell an incomplete story. Many people search, read and write about technology solely out of interest, with no intent to buy. Accordingly, the authors propose that traditional sources skew and bias the analysis. Not only because they include data from people without a vested interest but also because these analyses assume that everyone starts at the same knowledge point and then assesses the information in a linear manner. This can’t be the case. On the other hand, information coming directly from corporate leaders, such as in voluntary and involuntary disclosures, shareholder conference calls, etc., provides reliable insight because it contains more detail, it comes “straight from the horse’s mouth” so to speak, and the source has a vested interest.

“The major advantage of firm disclosures, over prior information gathering proxies, in measuring technology adoption is that they provide more detailed information.”

Firms disclose information voluntarily and/or because they are required to by the Securities and Exchange Commission (SEC). They may also use conference calls and other vehicles to voluntarily reveal their plans to adopt new technologies because they wish to signal to investors and the public that they are IT leaders, and/or expect to garner competitive advantage by moving on a promising technology early. Others might disclose their plans in order to signal to investors that they intend not to be left behind by competitors.

Likewise, start-ups and mature technology firms sometimes have an incentive to share their strategies. They might disclose their plans to integrate an emerging technology like Blockchain in order to differentiate themselves in a crowded market. And even where private firms would prefer to keep their intentions secret, they cannot do so once they file an IPO. Millions of mandatory disclosures of publicly traded firms reside in a searchable SEC database called EDGAR that dates back to 1993. This extensive data set, used by the researchers in their analyses, offers invaluable information about buyer demand and seller intent.

Generally, the researchers propose that buyer disclosures (voluntary and mandatory) will peak as a technology is leaving the innovator stage and seller disclosures will peak as the technology is purchased by early adopters. These peaks – first demand and then supply – will give way to declining disclosures and interest as an emerging technology moves from the innovator to the early adopter stage.

The Analysis

The researchers used web search, article and book title trend analysis combined with disclosure of corporate information, EDGAR searches of SEC filings, a review of relevant research, information from Blockchain industry consortia, and the Latent Dirichlet Allocation (LDA) machine learning algorithm to perform a natural language processing (NLP) analysis of the data and documents to test and validate their assumptions.

The researchers were careful to isolate Blockchain from associations with technologies that could cloud their results, such as cryptocurrencies (e.g., Bitcoin). They discarded evidence of interest in Blockchain as it relates solely to cryptocurrencies or other primary technologies. In other words, they only incorporated evidence of interest in the underlying technology – Blockchain.

Results

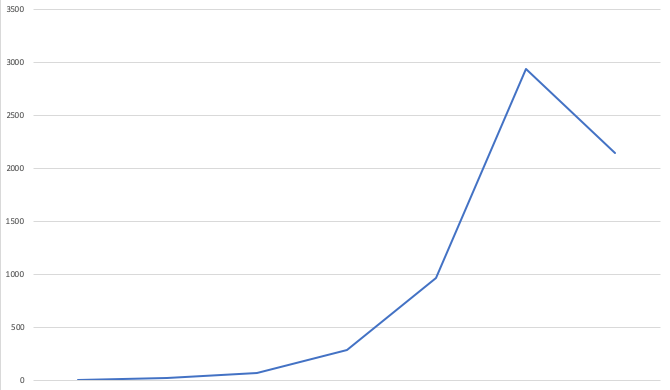

The researchers’ analysis of corporate disclosures and the other proxies described above revealed a consistent peak in Blockchain interest in 2018 followed by a decline in 2019 (Figure 2). Separately, the researchers examined disclosures, earnings conference calls and the other proxies against demand (buyers) and supply (incorporation of Blockchain into technology offerings). The spike in disclosures and interest followed by a drop fits the researchers’ expectations where an emerging technology is transitioning the innovator stage to the early adopter stage.

Figure 2 does not separate demand side disclosures and interest from the supply side. Logically, the researchers propose that demand-side interest peaks before supply. Their analysis bears this out. This, and results from the NLP performed by the LDA algorithm lend further support to the results above, namely that Blockchain adoption rates remain low; it is only now transitioning to the second stage of the adoption cycle: early adoption.

Importantly, however, the analysis reveals that corporate interest in Blockchain has untethered from Bitcoin and other cryptocurrencies. Organizations are now looking at Blockchain as a means to improve a variety of business processes.

Figure 2: Combined Results of Proxy Analyses.

Key Takeaways

- Just five years ago, interest in Blockchain was linked closely with cryptocurrencies. The researchers’ analyses – particularly from the LDA algorithm’s NLP – reveal that by 2018 and 2019, firms and suppliers showed almost three times as much interest in Blockchain for non-cryptocurrency business applications than they did for things like bitcoin. This suggests that Blockchain has reached the early adopter stage and may successfully cross the chasm, eventually living up to its expectations as a game changer.

- In combination with more traditional methods, the use of voluntary and mandatory corporate disclosures in SEC filings, IPOs and earnings conference calls is a novel and powerful technique that anyone can use. Corporate disclosures are plentiful, up-to-date, easily obtainable, and structured for analysis. Tools used by the authors enable efficient analyses, such as SeekEdgar which searches millions of SEC filings.

- The authors’ technique might be used to assess any emerging technology as it evolves, potentially offering actionable insights and early predictors for buyers and investors. Moreover, this capacity can be tested by studying past disclosures to track the adoption of established technologies like ERP.

Additional questions? Please forward any questions you may have about this research to Dr. Theo Stratopoulos at: tstratopoulos@uwaterloo.ca.