Eligibility

Contributions

How to join

Transferring to the UWaterloo Pension Plan

Naming a beneficiary

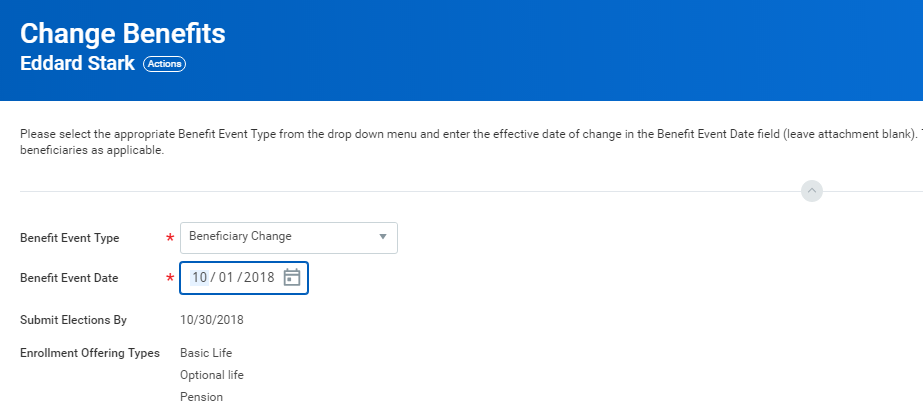

Changing your beneficiary designation

Log onto Workday to access the Benefits application:

- Click the Benefits button under Change.

- Select the Benefit Event Type.

- Click the Calendar icon to enter the date of the Benefit event.

- Attach required documents, if applicable.

- Click Submit.

- Click Open on the next screen to complete this task right away (or go to your inbox to complete).

- Complete and continue through all required screens. Check the I Agree checkbox, if required, to provide an electronic signature, confirming your changes.

- Click Submit.

- Click Done to complete the task or Print to launch a printable version of the summary for your records.

If the beneficiary you wish to designate is not already in Workday, you will be prompted to add a new beneficiary record.

As a wet signature is required to finalize your designation, you will receive a notification to print and complete a beneficiary designation form. The original signed copy must be returned to HR by campus mail. Please ensure the paper form matches the designation that you input in Workday.

If the beneficiary named is a person under the age of 18, it is strongly recommended that you name someone in trust for them. Also, note that spouses have certain entitlements under the pension plan. If you elect to designate someone in addition to or in place of your spouse as your pension beneficiary, we require a completed pre-retirement waiver form (PDF), signed by both you and your spouse.

Detailed instructions can be found in the beneficiary change instructions. Please contact hrhelp@uwaterloo.ca or extension 45935 for any questions.

Key terms

FTE: Full-Time Equivalent. 100% FTE means you work full-time.

YMPE: The year's maximum pensionable earnings (YMPE) and the year's additional maximum pensionable earnings (YAMPE) are defined in the Canada Pension Plan Act.

Base earnings: Basic monthly or weekly salary excluding overtime, reimbursement for expenses, shift premiums, special allowances, stipends and other like payments.

Spouse is defined as a person to whom the member is:

- Legally married, provided the member is not living separate and apart from that person; or

- Not legally married, but the member and that person are cohabiting continuously in a conjugal relationship for at least three years; or,

- Not legally married, but the member and that person are cohabiting in a conjugal relationship of some permanence, and are jointly the natural or adoptive parents of a child, both as defined in the Family Law Act, 1986 (Ontario).