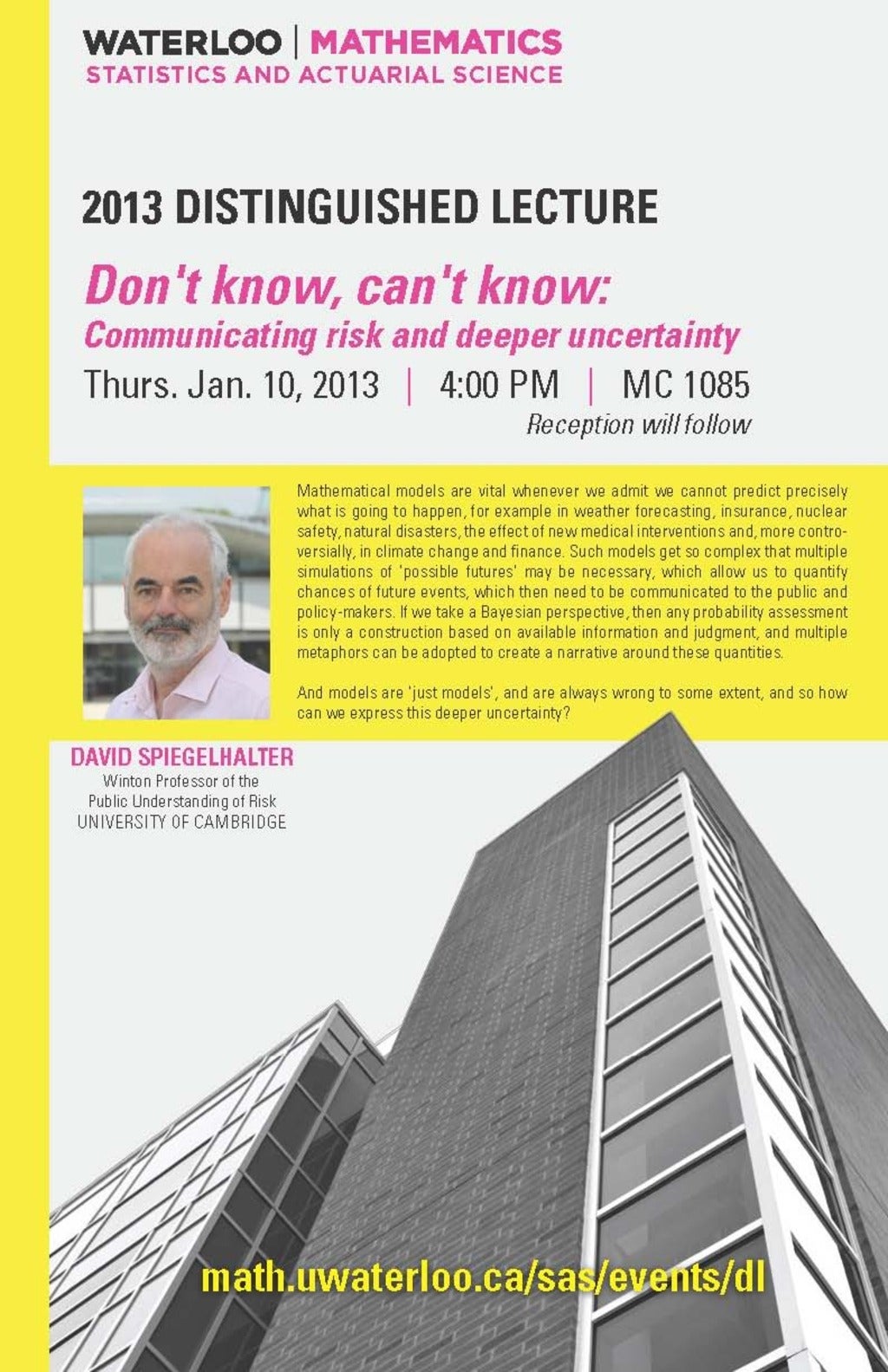

Thursday, January 10, 2013 4:00 pm

-

4:00 pm

EST (GMT -05:00)

First annual distinguished lecture by David Spiegelhalter

Don't know, can't know: Communicating risk and deeper uncertainty

David Spiegelhalter, Winton Professor of the Public Understanding of Risk, University of Cambridge

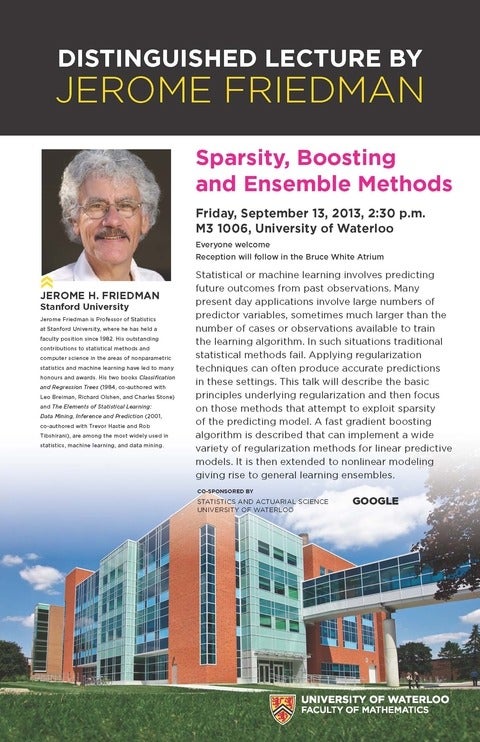

Statistical or machine learning involves predicting future outcomes from past observations. Many present day applications involve large numbers of predictor variables, sometimes much larger than the number of cases or observations available to train the learning algorithm. In such situations traditional statistical methods fail.

Statistical or machine learning involves predicting future outcomes from past observations. Many present day applications involve large numbers of predictor variables, sometimes much larger than the number of cases or observations available to train the learning algorithm. In such situations traditional statistical methods fail.

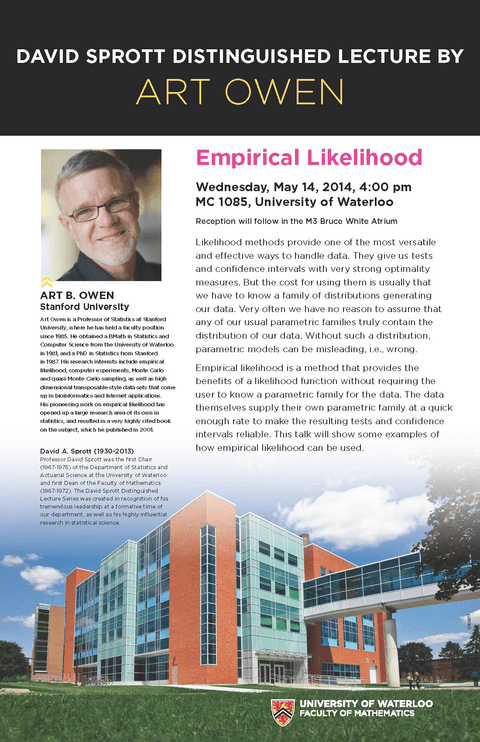

Likelihood methods provide one of the most versatile and effective ways to handle data. They give us tests and confidence intervals with very strong optimality measures. But the cost for using them is usually that we have to know a family of distributions generating our data.

Likelihood methods provide one of the most versatile and effective ways to handle data. They give us tests and confidence intervals with very strong optimality measures. But the cost for using them is usually that we have to know a family of distributions generating our data.

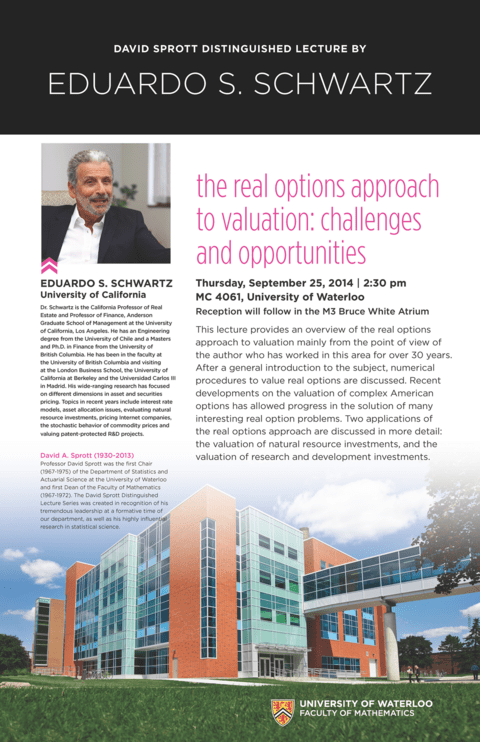

This lecture provides an overview of the real options approach to valuation mainly from the point of view of the author who has worked in this area for over 30 years. After a general introduction to the subject, numerical procedures to value real options are discussed.

This lecture provides an overview of the real options approach to valuation mainly from the point of view of the author who has worked in this area for over 30 years. After a general introduction to the subject, numerical procedures to value real options are discussed.